Rising Deductibles

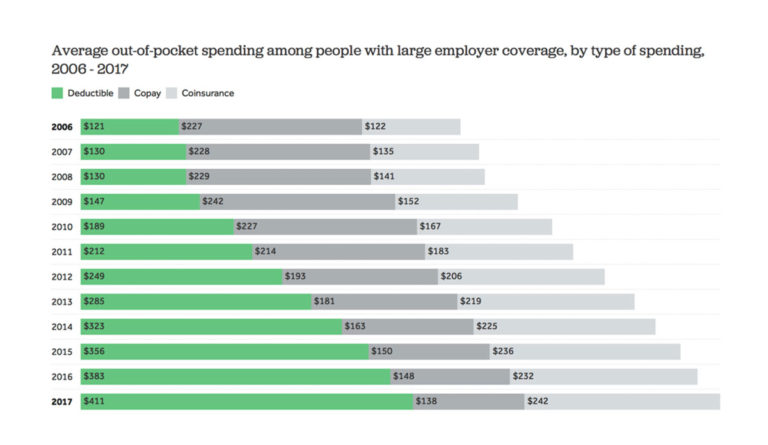

A recent analysis of out-of-pocket spending by the Kaiser Foundation found that between 2006 and 2017, deductibles increased as co-pays shrank.

Read Time: 2 minutes

Published:

Private health insurance carries a Holy Trinity of payment types in addition to one’s monthly premium: deductibles, co-pays, and co-insurance. For plans with deductibles, individuals must pay their own health care expense up to a specified amount before their insurance coverage begins. In a co-payment arrangement, a person agrees to pay a fixed dollar amount for each doctor visit or prescription drug purchased. With co-insurance arrangements, individuals pay a deductible and a percentage of the cost of any health service received. These personal payments make up “out-of-pocket” spending.

A recent analysis of out-of-pocket spending by the Kaiser Foundation found that between 2006 and 2017, deductibles increased as co-pays shrank. As depicted in the graph, spending on deductibles nearly quadrupled from $121 to $411. In the same time period, co-payments fell from $227 to $138.

In 2006, deductibles accounted for only 28.8% of health insurance cost-sharing. By 2016, this percentage had risen to 51.7% of cost-sharing payments. This year, nearly half of American families with health coverage had deductibles of $3,000 or higher.

As deductibles rise, fewer people are able to meet the financial requirements. The pricey upfront costs of deductible plans also push people to delay much-needed care or forego it altogether.

Databyte via Deductible Relief Day: How rising deductibles are affecting people with employer coverage. Peterson-Kaiser Health System Tracker, 2019.