House Republicans recently released a new plan to replace Obamacare. It’s hard to say exactly what effects it would have because the plan is more of an outline without legislative language or many details. Even so, today I take a look at the evidence we have about the likely effects of the key parts of the outline. I try to be fair, acknowledging that the Republican goal for health reform is fundamentally different than what the Democrats tried to achieve with the ACA’s passage seven years ago. The point isn’t to cover as many people, but to reduce the role of the federal government and government spending in health care. So for each component I describe a pro and a con, why the House Republicans like the idea and why opponents don’t.

1) Medicaid block grants

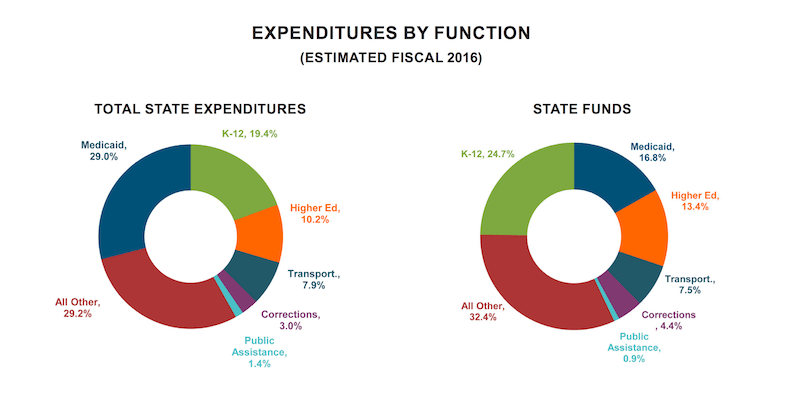

Pro – Medicaid is now the single largest budget item in most states, accounting for more than a quarter of all state expenditures. This is of great concern to state leaders trying to get a handle on their budgets so they will have enough money for other things like transportation and education. Of course, when you factor in how much of this money comes from the federal government, states are really spending more like 17% of their own funds on Medicaid. But that is still a lot of money that they have very little control over. Republicans also don’t like that the federal government effectively writes a blank check to states for Medicaid, with very little ability to reduce spending. The federal burden has only increased with the ACA’s promise to pay at least 90% of the costs of enrollees in the expansion population. Block grants would solve these problems by giving states a fixed amount of money to spend on Medicaid. The federal government would no longer be a blank check and states would have greater flexibility on how to spend the federal dollars they receive for Medicaid.

Con – There are three primary ways that states can reduce spending on Medicaid as they try to manage a block grant they receive from the federal government: 1) reduce the number of people enrolled in the program, 2) make the benefits less comprehensive, and 3) pay health care providers less for their services. Any of the three would lead to decreased access to care for vulnerable people who cannot afford another option.

2) Health savings accounts

Pro – Individuals are able to set aside money, often tax-free, to be used at their discretion to pay towards health care expenses. Unused money rolls over to subsequent years, meaning that people who manage their health savings account well can accumulate a nice balance. The theory goes that because people have a larger stake, they will be more cost conscious and not spend as much and health care costs will be contained. There is insurance that kicks in after a large deductible is paid from the HSA, and the premium is relatively low because the deductible is so high.

Con – People save money in an HSA by delaying and deferring care. That is fine as long as the care they are delaying is unnecessary, but it leads to bad health and financial outcomes if they are delaying necessary or preventative care. One of the major criticisms of Obamacare is the large number of plans sold on the exchange with high deductibles. It would therefore be ironic if one of the major coverage components of the ACA replacement plan was explicitly based on the idea of high deductibles.

3) High risk pools

Pro – Its harder for me to find the pro here. I guess high risk pools are better than nothing for people who are pushed out of an ACA plan but can’t get insurance another way because of costs or pre-existing conditions.

Con – high risk pools face actuarial math that doesn’t add up by trying to pool the sickest and least insurable people together. Analysis by Jean Hall published by the Commonwealth Fund shows that they are 1) extremely expensive to administer, 2) prohibitively expensive for consumers, with very high premiums and deductibles, and 3) offer limited coverage, often with annual and lifetime caps. We are talking about deductibles as high as $25,000 and yearly coverage limits of $75,000. Once again, it would be ironic if high risk pools are touted by opponents of the ACA as the way forward. Technically these people will have coverage, but it won’t be very good and won’t protect them from medical debt.

4) Age-based tax credits

Pro – Right now the ACA gives tax credits to people between 100-400% of the federal poverty level so that they can purchase insurance. The tax credit is on a sliding scale based on income so that people with less money receive the greatest help. The House Republican plan would change this so that everyone receives a tax credit, regardless of income. The amount would be based on age so that older people, whose health care costs are presumably more expensive, would receive more than younger people. As Margot Sanger-Katz of the NY Times points out, this means that multi-millionaire Secretary of State Rex Tillerson would receive the same level of help as another 64 year old living in poverty. This approach would be simpler to administer and would eliminate an incentive that younger people might have faced to not work harder and earn for fear that they would receive less help.

Con – The 64 year old living in poverty has much greater need than Rex Tillerson. Young people often don’t make enough money to make up the difference between the tax credit and the cost of coverage. Without the requirement that everyone be covered, many young people will likely gamble by foregoing insurance. This hurts them when they get sick and weakens risk pools, driving up costs for everyone else.

As I wrote two weeks ago, the metric we should be using to evaluate alternatives in the debate over health reform is not whether a plan solves all problems, but whether it leaves us with a better set of problems. You can decide for yourself, but I think the evidence shows that the House Republican plan leaves us with a worse set of problems.

Feature image: Ron Cogswell, House of Representatives Building and the East Portico of the U.S. Capitol – Washington (DC) January 2013, used under CC BY 2.0/cropped from original

Graph from the NASBO State Expenditure Report